Information for COVID-19 Changes

Payroll Tax Deferment - Issued August 28, 2020

The Department of Treasury and Internal Revenue Service, on August 28, 2020, issued guidance implementing the Presidential Memorandum issued on Aug. 8, 2020, allowing employers to defer withholding and payment of the employee’s portion of the Social Security tax if the employee’s wages are below a certain amount.

Notice 2020-65, posted today on IRS.gov, makes relief available for employers and generally applies to wages paid starting Sept. 1, 2020, through Dec. 31, 2020.

Applicable Wages means wages as defined in section 3121(a) or compensation as defined in section 3231(e)3 paid to an employee on a pay date during the period beginning on September 1, 2020, and ending on December 31, 2020, but only if the amount of such wages or compensation paid for a bi-weekly pay period is less than the threshold amount of $4,000, or the equivalent threshold amount with respect to other pay periods. The determination of Applicable Wages is made on a pay period-by-pay period basis.

An Affected Taxpayer must withhold and pay the total Applicable Taxes that the Affected Taxpayer deferred under this notice ratably from wages and compensation paid between January 1, 2021 and April 30, 2021 or interest, penalties, and additions to tax will begin to accrue on May 1, 2021, with respect to any unpaid Applicable Taxes. If necessary, the Affected Taxpayer may make arrangements to otherwise collect the total Applicable Taxes from the employee.

Recommendation for Implementation of this Deferment

This deferment is voluntary so we recommend that whether or not you defer the employee side Social Security Tax be discussed and decided with your employees. It is important to remember that the responsibility to remit deferred taxes by May 1, 2021, lies with the employer (Affected Taxpayer), according to this guidance. There are still many unanswered questions regarding this deferment so please be aware that there may be changes or updates in the days and weeks to come.

Important issues to keep in mind:

- You, as the employer, are responsible for remitting the deferred employee side Social Security Tax. According to the guidance issued by the IRS, the employer is the "Affected Taxpayer." This is an important factor to consider for this deferment.

- If the full amount of the deferred tax is not repaid, penalties, interest, and additions will start to accrue on May 1, 2021. This obligation falls to the employer as the Affected Taxpayer regardless of whether the employee is with the company or not after 2020.

- If you, the employer, decide to repay the deferred tax in 2021, once you have repaid the deferred amount, the US SS amount will be zero when you calculate your next payroll. This is because C21 thinks that you have overpaid the Employee Side Social Security Tax for 2021 and is attempting to compensate. You will need to manually enter the correct employee side US SS Tax for each payroll for the rest of 2021.

- Only employees that earn up to but not more than $4,000 bi-weekly in 2020 are eligible for this deferment.

Even though the guidance issued by the Secretary of the Treasury provides you with a repayment period of January 1, 2021 through April 30, 2021, we recommend these taxes be paid before the first payroll in 2021. The reason we recommend this is that, if you choose to deduct the owed taxes from wages in 2021, you will need to make adjustments to your US SS Tax for relevant employees for the rest of the year in each Calculate Payroll procedure. This may lead to confusion and complications in your payrolls. Please keep this in mind before deciding how to proceed.

How to defer employee side Social Security Tax

In order to increase the amount of an employee paycheck by the amount of the employee side Social Security Tax due, you can edit the amount listed in the US SS box during the Calculate Payroll process. If you delete the amount calculated by the system, this will eliminate the employee side portion of the US SS Payroll Tax. You will need to manually make this change for each eligible employee during the Calculate Payroll procedure. The next payroll will show the amount due for the current payroll as well as the previous payroll that was eliminated. The full amount will show during every Calculate Payroll procedure until the first payroll in 2021.

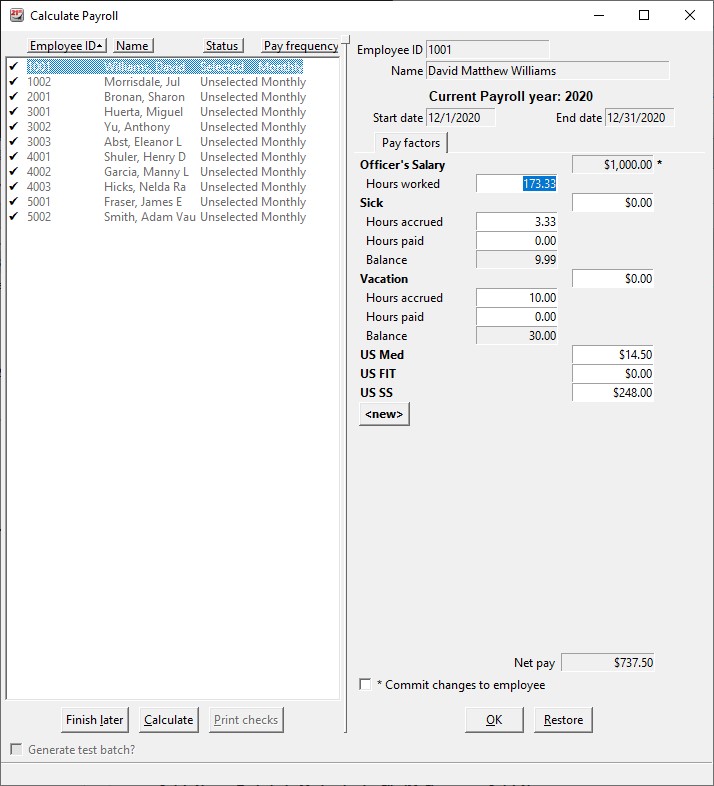

Before you process 2021 payrolls, if the employee would like to pay the amount back, you can run Calculate Payroll in 2020 and leave the amount due for the employee side Social Security Tax as it is. The following screenshot shows a Payroll calculated in December for an employee that excluded the employee side SS Tax from previous payrolls. As you can see, the amount of $248.00 (4 x $62.00) is listed in the US SS box for a monthly salary of $1000.00. During a normal Calculate Payroll session, this amount would be $62.00 (6.2%) for this salary. This Payroll shows the accumulated amount of the Employee side US SS Tax due for each Payroll from September 1, 2020 through December 31, 2020.

Continuing with the above example, once you start a Payroll for 2021, the amount will show $62.00 for a $1000.00 salary. The deferred amount will no longer be reflected. If you and your employee have decided to repay the amount in 2021, you can edit the US SS amount to reflect the amount you wish to pay. For example, if you would like to pay $62.00 extra for each monthly payroll for $1000.00 salary from January through April 2021, you would change the amount to $124.00 each payroll. That would reflect the 6.2% tax due for the current payroll and $62.00 from the deferred amount from payrolls in 2020. You can do this for each month until May 2021.

If you have any questions or require assistance regarding this matter, please contact us.